The Art Basel and UBS Art Market Report recorded a 12% decline in the global art market in 2024, a downturn that has accelerated the use of art-backed lending. This decline parallels the increasing size of the art-backed loan market, which is expected to increase by 20%, from $40 billion to $50 billion by 2027 (Deloitte Private and ArtTactic Art Report). The spike in loans is due to collectors’ reluctance to sell at low prices and adhere to the sentiment of the market. These loans are a way to create “liquidity out of something that is just sitting there”, according to Nishi Somaiya, the Global Head of Private Banking Lending and Deposits at Goldman Sachs. The normalization of borrowing is significant among ultra-high-net-worth collectors. According to the Art Basel and UBS Survey from 2023, 43% of high-net-worth collectors have used credit or loans to buy art, whilst an average of 29% of collection value was financed through credit among users. Approximately one third of art is being financed similarly to credit card and auto loan institutions. Borrowing offers flexibility, diversification, and liquidity without relinquishing ownership, entering a new era of “Art Credit.”

The growing integration of finance introduces new vulnerabilities, namely valuation and liquidity concerns. Recent reporting from the Financial Times highlights rising defaults and margin calls as prices soften. Margin calls are atypical in this realm and signal a warning call. Art valuations can shift dramatically depending on market sentiment.

Art does not trade continuously like stocks and is increasingly volatile, raising a central question: as artworks become financial instruments, how stable is the system built around them?

Despite unpredictability, some auction houses are now generating revenue not only from selling art but from lending against it, crafting their own financial systems.

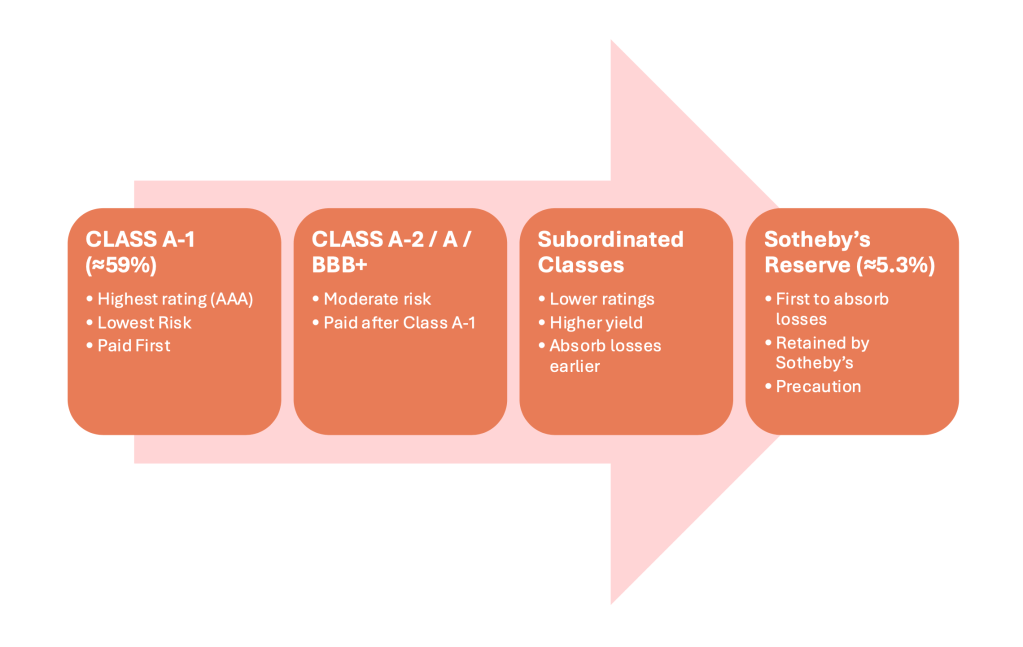

In 2024, Sotheby’s Financial Services launched a $700 million securitization backed by loans secured against art and luxury collections: Sotheby’s ArtFi Master Trust. It was a first of its kind in the industry and remains a landmark among art finance institutions. The trust works by giving loans to collectors using artworks as collateral and bundling the loans together. These loans are then turned into asset-backed securities (ABS) and sold to institutional investors. Simply, loans are turned into a portfolio, converted to bonds, and sold to investors. The loan pool consists of 89 loans, accounting for 2,484 works of fine art and collectibles. It is separated into five classes of securities ranging from Class A-1 to triple B, offering a hierarchy that attracts both conservative and yield-seeking investors. By selling securities, Sotheby’s is able to free up capital and tap into institutional investors. The result: Sotheby’s has freed up over $2 billion in funding capacity, a feat that Ron Elimelekh, co-head of Sotheby’s Financial Services, states have “help[ed] to further our mission of unlocking the power of our clients’ collections.”

Why then, if the trust has proven to be so successful, haven’t other art finance firms followed into the securities realm? The answer is knowledge. Few lenders have the expertise needed to evaluate art and collectibles. They lack historical data and professional evaluation to enter the market. Sotheby’s has an archive unmatched by other institutions that puts it at the forefront of art market research and predictability. With decades of empirical data, the company can make educated decisions on value despite unpredictable markets. In the case of collateral, Sotheby’s reserved a class representing 5.3% of the trust which would absorb the first losses in the transaction. Sotheby’s securitization marks a turning point where artworks no longer function only as cultural objects, but as financial assets. Will other institutions be able to follow in their tracks? More so, how can the aggregation and triangulation of historical data allow for expansion of art security funds?

Sources:

https://www.ft.com/content/45b266f5-a16e-4656-a7cd-b7a1c08f1fea

https://www.ft.com/content/b001c29d-e515-4907-bf56-a8477201e79f

Leave a comment